From Scratch to SOX-Compliant in 6 Months: An Executive Guide

Building a

robust SOX compliance program

from scratch doesn’t require massive headcount or runaway audit fees. Discover how to transition from

zero documented controls

to

100% audit readiness

in just six months.

SOX Execution Resources

Move beyond the basic compliance box. This checklist provides a practical framework to scale securely and achieve IPO readiness. Establish firm governance for AI tools, target the root causes of scope bloat, and clear the path for total operational stability.

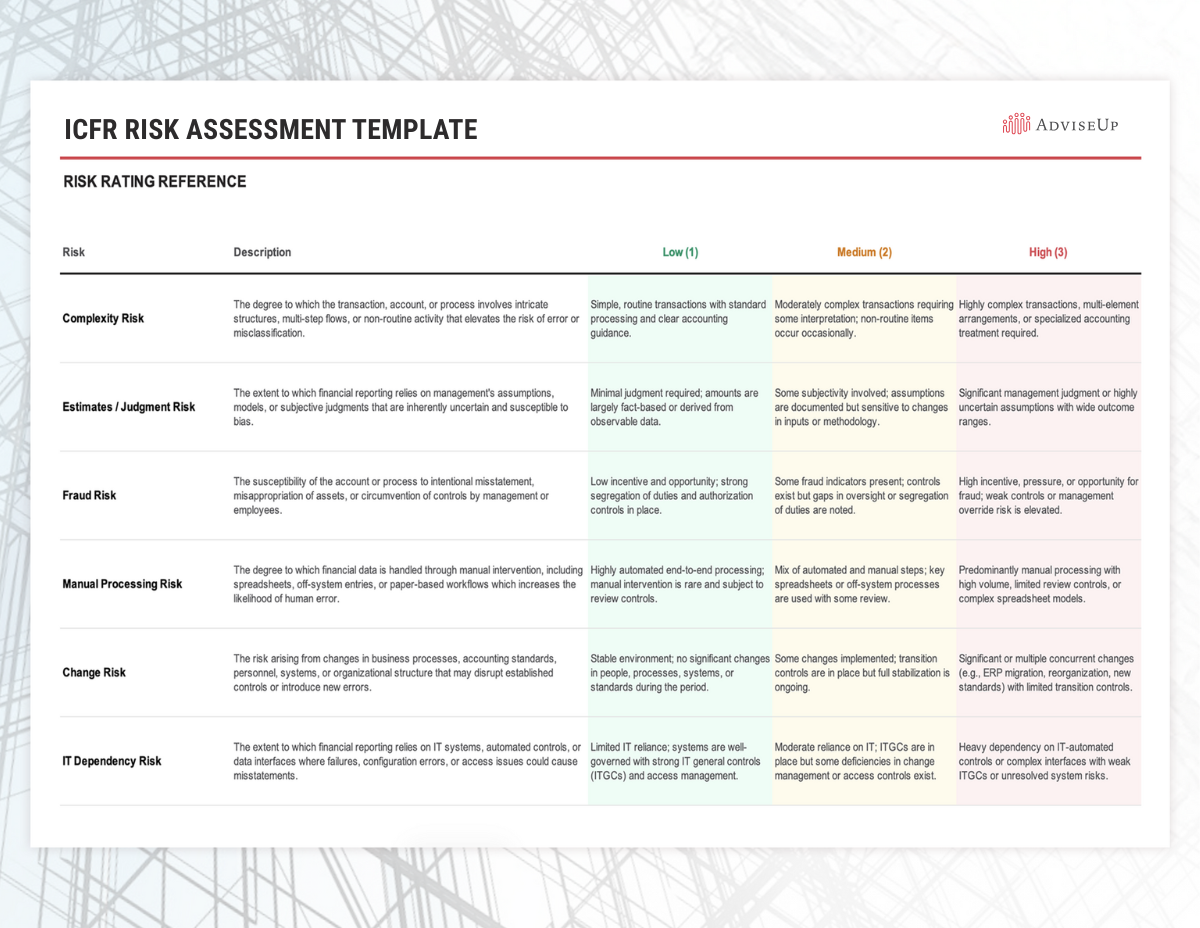

Build an optimized compliance engine. Use this template to establish a rigorous process for evaluating financial accounts. Perfect your scoping methodology by balancing quantitative materiality with qualitative transaction risks, ensuring your organization remains resilient and prepared for any audit.

Your company is preparing for its first SOX audit, and suddenly everyone wants answers. Which systems are in scope? Who owns the controls? How much documentation do we actually need? Six months sounds like plenty of time, until you realize you're starting from scratch.

It doesn't have to become an expensive, overly complicated project. With the right approach, six months is enough to build a practical SOX program that supports the business instead of slowing it down.

After years of leading internal audit, accounting, and SOX compliance initiatives, we’ve noticed a frustrating trend: internal controls are frequently treated as a bureaucratic compliance exercise. Those compliance exercises become a checkbox that external auditors require, and management rushes to complete them just to pass the annual audit.

When treated this way, the real value of controls—the systemic risks they mitigate, and the strategic decisions they protect—is lost. Worse yet, the cost of maintaining these programs can often be very high, especially when working with the big audit firms. Companies routinely spend significant capital maintaining clunky, over-scoped frameworks, while friction builds between operations and compliance, and external audit fees continue to skyrocket.

SOX programs do not have to be a resource drain. By focusing on smart design and aggressive scope management, we recently helped a rapidly growing mobile healthcare provider optimize their framework and cut their SOX compliance fees by 50%.

Read the full cost-reduction case study.

A strong internal control framework, when designed correctly, does far more than prevent financial reporting errors. It protects corporate assets, flags operational risks before they become financial surprises, and gives executive leadership confidence in their data without breaking the bank. In today’s AI era, they will become some of your best guardrails to protect you against hallucination and other issues AI models are currently introducing to companies.

Whether you are a CFO building a SOX program from scratch or a CAE looking for outsourced muscle to scale an existing framework, here is how to bridge the gap between theoretical compliance and high-performance, cost-effective control design.

The 5 Pillars of an Audit-Ready Framework

While the Committee of Sponsoring Organizations (COSO) outlines five core components for internal control, a finance leader needs to look past the textbook definitions and focus on practical execution.

1. Control Environment (Setting the Tone)

Often referred to as "the tone at the top," this is the foundation of your entire program. If senior leadership views controls as a nuisance, the rest of the organization will follow suit. A weak control environment is the fastest route to a material weakness. True control culture requires establishing clear accountability, robust organizational structures, and defined authority limits from day one.

2. Risk Assessment (Scoping for Materiality)

A common pitfall is trying to control everything, which is precisely why SOX compliance costs spiral out of control. An expert risk assessment focuses strictly on materiality and Financial Statement Line Items (FSLIs) that carry a higher risk of material misstatement. Management must systematically evaluate what could go wrong, analyze quantitative and qualitative data, and anticipate how business changes will impact financial reporting.

3. Control Activities (Smart Design vs. Resource Drain)

This is where the actual work happens: through preventive and detective controls, segregation of duties (SoD), and automated workflows.

For transactional controls, look for localized checks, like implementing automated, threshold-based approval workflows within your ERP for customer invoices. Strong segregation of duties (SoD) is one of the most effective ways to reduce fraud risk, since it prevents a single individual from controlling a critical process end-to-end.

Every control activity should be formal, documented in writing, and strictly balanced process efficiency against the cost of compliance.

4. Information and Communication (Overcoming Culture Shock)

Even the best control design will fail if it lives in a silo. When building or scaling a program, change management is critical. Process owners must understand not just how to execute a control, but exactly why they are doing it, and how to preserve the Information Produced by Entity (IPE) to demonstrate the completeness and accuracy of key reports and spreadsheets. If the execution trail isn't documented cleanly, to an auditor, it didn't happen.

5. Monitoring (Continuous Evaluation)

Internal controls are a living system, not a one-time implementation. Management must continuously monitor compliance through ongoing evaluations, supported by risk or internal audit teams. Testing exceptions should be treated as data points to optimize the system, allowing leadership to remediate design or operating deficiencies long before the year-end audit window closes.

Case Study: Rapid SOX Deployment in Action

To see these pillars in action, look at how we supported the UK subsidiary of a US publicly traded healthcare company. Confronted with their first year of SOX compliance, they had no documented controls, widespread system fragmentation, and only six months to achieve compliance before year-end testing.

Designing a Program That Outlasts the Audit

An effective internal control framework is one of the smartest investments an organization can make. Beyond protecting your company from regulatory penalties and runaway external audit fees, a lean internal control system safeguards your assets, optimizes operations, reduces fraud exposure, and provides reasonable assurance over financial reporting reliability and accuracy.

But understanding the COSO framework in theory is very different from building a sustainable compliance program that can withstand external audit scrutiny.

Ready to Build a SOX Program That Actually Works?

Don't let your compliance program become a drain on your internal resources. Download our Executive SOX Readiness & Pitfall Checklist to identify critical gaps in your current environment and avoid the common traps that drive up audit fees.

If you're preparing for your first SOX audit or IPO, we can help you quickly identify where you stand, prioritize the gaps that matter most, and build a practical roadmap to audit readiness.